INTRODUCTION IN PUBLIC FINANCE

What is Public Finance

As a young graduate from Somalia’s prestigious Institute of Accountancy, Public Finance, and Management, SIDAM Institute, I was always fascinated with financial figures and reports, whether from the private sector or the government. Understanding budgets and financial forecasts is essential for business planning, budgeting, business operations, and proper funding. They simply help leaders and outside stakeholders make better choices.

As I grew older and became a qualified instructor at local universities, I noticed that many students were still fascinated by the subject of public finance. However, by the time they start the course, they often feel confused about which academic discipline it belongs to. Reactions can vary widely, as they depend on students’ backgrounds, experiences in public life, and personal expectations. Some students are eager to learn about how government policies impact the economy and society at large. They are thrilled to learn, for the first time, what tax systems, public expenditures, and economic efficiency truly entail.

Many students found the topic challenging due to its technical nature, which involves economics, finance, and policy analysis. Some felt overwhelmed by the complexity of the concepts and the mathematical models presented. As a junior student at SIDAM Institute, I was fascinated by how the public finance course could lead to a better understanding of real-world applications, particularly regarding government budgets and public projects. My expectations were further broadened as I was exposed to policy debates, social welfare programs, and government interventions in the market economy. Those of us already working in the public sector were motivated by the positive impact that public finance courses can have on society through effective policy analysis and financial management.

Based on that background, it is imperative to start with the broad definition of public finance as a branch of economics that deals with the financial activities of the state or government at national, state, and local levels. It covers a wide spectrum of areas such as income and expenditure, government spending theories and practices, and ways to raise government.

The term “public finance” is derived from the words “public” and “finance.” “Public” refers to the government or state, while “finance” refers to money resources, including income and expenditures. Therefore, public finance involves the systematic study of how public authorities generate revenue and manage expenses. This field is a branch of economics and focuses on the income and expenditures of all levels of government. It also examines how governments acquire and allocate financial and real resources in a market economy.

The Scope of Public Finance

Public income refers to money earned by the government, primarily through the taxation system. Public expenditure, on the other hand, is money spent by government entities on infrastructure, defence, social services, and other areas. When public expenditure exceeds public income, the government borrows money from the public, other countries, or world organizations like the World Bank. This borrowed money is known as public debt. Financial administration in public finance involves managing public income, expenditure, and debt.

The function of Public Finance

Public finance is essential for managing a nation’s economy and ensuring the well-being of its citizens. Here are some key functions of public finance:

- The allocation function in the economy deals with how private goods are exclusive to those who pay for them (e.g., a car). In contrast, public goods are nonexclusive and benefit everyone, regardless of payment (e.g., roads).

- Public finance’s distribution function aims to reduce income and wealth disparities within a country through measures such as progressive taxation, affordable housing, and healthcare.

- The stabilisation function of public finance aims to mitigate the economic instability caused by booms and depressions. This involves strategies such as running a budget deficit during a depression and a budget surplus during a boom to achieve economic stability.

Functions of Public Institutions

Public institutions play a crucial role in the society and maintaining order. Governments carry out specific functions that can be categorized into two main areas:

- Obligatory functions: These include protecting the country from external aggression and internal disturbances and maintaining peace and security.

- Optional functions: These are the functions that a country can survive without. The government requires funding from the public to carry out all these functions effectively.

Public Finance vs Private Finance

Public finance is the study of managing money, including income, expenses, borrowing, and financial administration for private individuals or institutions.

Private finance can be categorized into two groups: personal finance and business finance. Personal finance involves optimizing finances for individuals, such as people, families, and single consumers. On the other hand, business finance involves optimizing finances for organizations.

Similarities between Private Finance & Public Finance

Public finance and private, while distinct in their objectives and scope, share many similarities including the following:

- Maximizing Advantage – to attain the maximum benefit from expenditures.

- Income Precedence – In personal finance, income should come before spending. In public finance, revenue must be generated before expenses can be covered.

- Resource Scarcity – Both individuals and the state must allocate their limited resources to meet various needs.

- Borrowing – When expenses exceed revenue, both individuals and the state may need to borrow money.

- Balancing Income and Expenditure – Both public and private entities need to balance their income and expenses.

Dissimilarities between Private Finance & Public Finance

Despite the aforementioned similarities, the key difference lies in their primary objectives. Public finance aims to maximize social welfare and economic stability while private finance focuses on maximizing individual and corporate wealth and profitability. The differences can be summarized briefly as follows::

- Determining Expenditure: Governments first determine the amount of money they need to spend on different areas in order to fulfill their obligations. They then try to find the resources to meet this expenditure. On the other hand, individuals first consider their income and then determine how much they can spend.

- Credit Status: Private individuals have limited credit and can only borrow a limited amount of money from limited sources within the economy. Governments, on the other hand, enjoy a high degree of credit in the market and can borrow large amounts from both their citizens and foreign sources.

- Right to Print Currency: Governments have the authority to print legal tender notes to cover budget deficits, which are not available to private individuals.

- Nature of Budget: Surplus budgets are favourable for private individuals as they spend less than their income and can save. However, governments generally prefer deficit budgets as they spend more than their income.

- Coercive Methods: Governments can use coercive methods to collect revenue, and citizens cannot refuse to pay taxes if they are liable. Private individuals cannot use force to earn income and must do so through their own efforts.

- Secrecy of the Budget: Individual budgets are private and shrouded in mystery, while government budgets are publicly presented, discussed, and subject to criticism in a democratic country.

- Compulsory Character: Public authorities cannot avoid or postpone certain expenditures, while private finances are voluntary and individuals can plan to postpone their expenditures.

- Pattern of Expenditure: Government public expenditure is governed by deliberate economic policy and considers the country’s economic, social, and political requirements. Private finance is profit-oriented and influenced by personal needs, habits, fashion, and status.

- Time and Objectives: Public finance allocates resources to projects that yield future returns, with the objective of securing maximum social advantage. Private finance has short-term considerations and aims to fulfill private interests.

- Effect on Economy: Public expenditure has a tremendous effect on the economy due to its large scale, while private expenditure has only a marginal effect.

Objectives of Public Finance

Public Finance has key several objectives that aim to ensure the well-being and economic stability of a country. To define such objectives, one must remember the main points which include securing adjustments in the allocation of resources, reducing economic inequalities, maintaining economic stability, achieving full employment, accelerating economic development, securing distributive justice, achieving maximum utilization of resources, and increasing the rate of capital formation by raising the rate of saving and investment. By focusing on these objectives, public finance seeks to foster a more equitable and prosperous society.

Components of Public Finance

In the real world, public finance encompasses various components that are essential in managing a country’s economy and fiscal policies. Thus, public finance involves the management of government income from all sources, government spending, public budget analysis, allocation of state finances, government loans from both domestic and foreign sources, and the use of government revenue and expenditure to promote economic stability, growth, full employment, and efficient resource utilization.

These components work together to ensure effective management of the country’s finances, economic stability and growth.

Role of Public Finance

Public finance plays a crucial role in shaping a country’s economic and social landscape. It increases the rate of capital formation, boosts economic growth, achieves optimal resource utilization, attains full employment, decreases economic inequalities, and counteracts inflation. In summary, public finance is essential for maintaining a balanced, stable, and prosperous economy, ensuring the well-being of all citizens, and promoting social equity.

Sources of Public Revenues

Public revenue refers to the income of the government from all sources, which are essential for funding government operations and public services. In a narrow sense, it includes only those sources of income described as revenue resources (tax, fees, fines), or in a wider sense, it encompasses all income and receipts (including loans raised to be repaid). The sources by which the government earns income are classified into:

- Tax Revenue

- Non-Tax Revenue

- Administrative Revenues

- Commercial Revenues

- Other Revenues

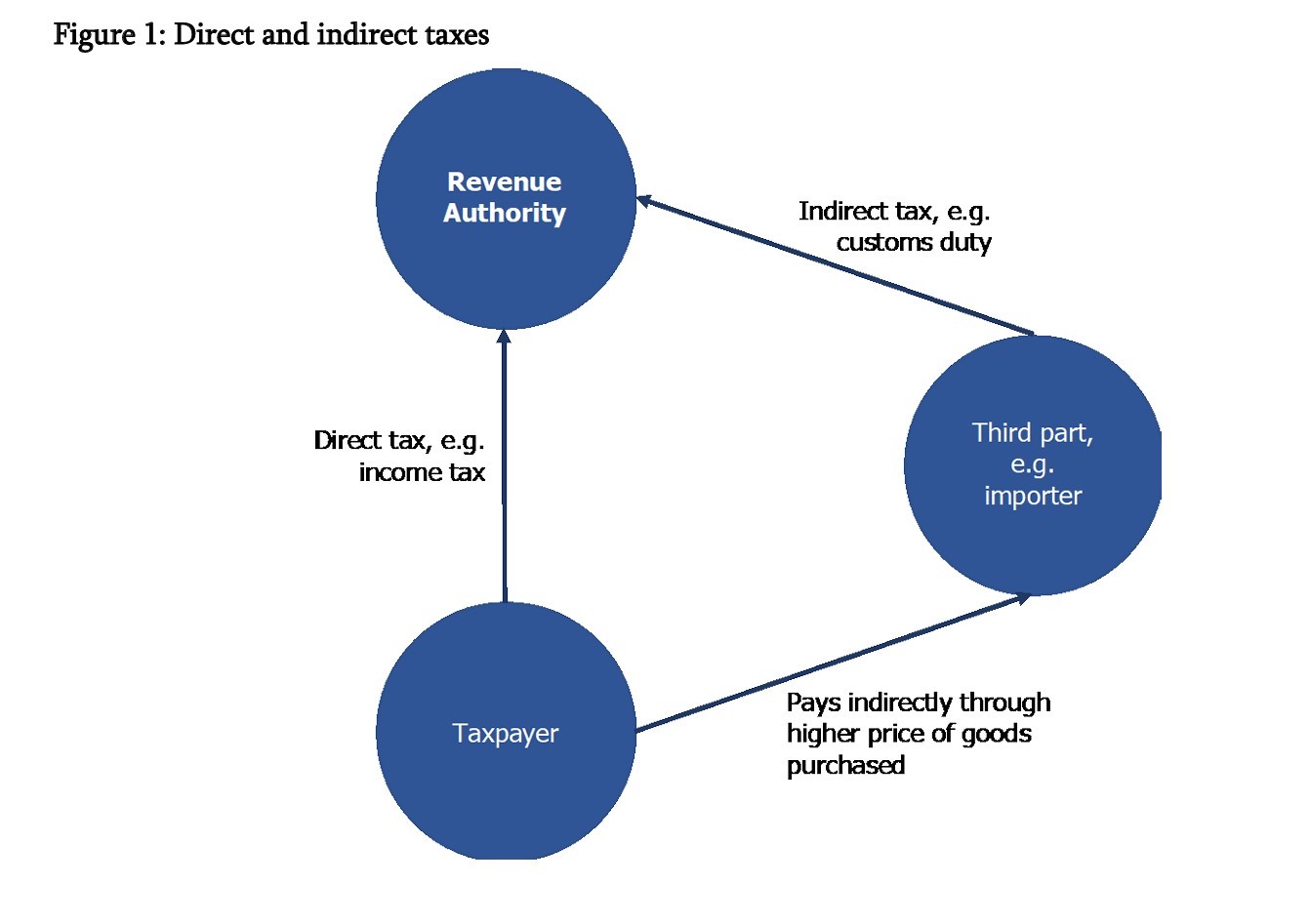

These diverse sources of public revenue help governments fund their activities and provide essential services to the citizens. Tax revenue is the income obtained by the government through taxation. Taxes are mandatory contributions imposed by the state to cover expenses in the “common interest of all citizens”. Tax revenue can be categorized into two types: Direct Taxes and Indirect Taxes.

Direct Taxes are taxes that the payer bears the burden of and cannot shift to any other person (such as income tax, wealth tax, and gift tax). Indirect Taxes, on the other hand, are taxes that the payer can shift to others. For example, if a sales tax or VAT is imposed on clothes, the producer or dealer who pays it passes it on to the next taxpayer.

Somalia/Puntland State Direct/Indirect Taxes (Inland Revenue Department)

The Inland Revenue Department has two main sections: direct tax and indirect tax. Direct taxes include property tax, employee tax, and business income tax. Indirect taxes include sales tax, stamp tax, road tax, registration tax, production and excise tax, and other indirect taxes.

Source: Puntland PFM Education and Training: DRM Workbook 2

Tax Revenues

Let’s consider an example based on a GST rate of 5%. A shopkeeper purchased a television from a manufacturer and paid Sh12,600, which includes GST (Sh12,000 plus GST @5% Sh 600) to the manufacturer.

The shopkeeper then sold the television set for Sh15,000. When selling, the shopkeeper added 5% of Sh15,000 (Sh750), so the total price to the customer, including GST, was Sh15,750 (sale price *1.05).

Out of the Sh15,750 paid by the end user, the shopkeeper kept Sh15,000 and paid Sh750 (Net of the GST paid*) to the IRD. The shopkeeper will claim back the GST he paid on the television (Sh600), so the net GST he will pay over is Sh750—Sh600 = Sh150. Then, the consumer who bought the TV hired an electrician to install it. The electrician charged Sh400 for the service and added 5% GST (Sh20), bringing the total charge to Sh420.

Since the electrician had paid no GST to anyone, there was nothing to deduct, and he paid the full Sh20 to the IRD.

Non-Tax Revenues

Non-tax revenue refers to public income raised by the government from sources other than taxes in the economy.

- Administrative revenues include fees (payments charged to cover the administrative cost of services), special assessments (compulsory contributions based on the special benefits derived from the cost of special improvements or increases in property values due to the construction of roads), fines and penalties (punishments imposed for the infringement of the law), and forfeitures (penalties imposed by courts for failing to appear).

- Non-Tax Revenues

- Commercial revenues refer to the income earned by public sector enterprises through selling goods or services to citizens. This includes commercial and industrial enterprises such as utilities, railways, post services, transport, and other public sector industries.

- Other revenues include gifts, grants, and donations from organizations like the IMF, citizens, and foreign governments. Additionally, government properties such as public land, buildings, mines, forests, and fisheries contribute to government revenue. Public borrowings, both internally and externally from organizations like the IMF, World Bank, and African Development Bank, are also sources of revenue. Tributes and indemnities received from foreign countries as a result of war or aggression, as well as the recovery of loans from debtors, also contribute to government revenue. Finally, miscellaneous sources such as revenue from auctioning confiscated items are also considered in government revenue.

Public Expenditure

Public authorities, including central, state, and local governments, incur expenditures to protect citizens and promote their economic and social well-being. Public expenditures are divided into two main categories: revenue expenditures and capital expenditures. Public expenditures and revenues are intrinsically linked as they play crucial roles in a government’s fiscal management.

Revenue expenditures include government spending on day-to-day administration, civil expenditures, economic or public debt services, defence expenditures, grant aid to other governments, and miscellaneous expenditures.

On the other hand, capital expenditure involves spending on creating permanent revenue-yielding assets, such as developmental and non-developmental expenditures, repayment of public debts, and loans/advances to other governments.

In the real world, governments strive to balance public expenditures with public revenues to maintain fiscal stability. A balanced budget is achieved when total revenues equal total expenditures. When public spending exceeds public revenues, a budget deficit arises, which often necessitates government borrowing, leading to public debt. Conversely, when public revenues surpass public expenditures, a budget surplus occurs. This surplus can be used to pay down existing debts, save for future needs, or invest in public projects. In summary, balancing public revenues and expenditures is crucial for achieving fiscal sustainability, economic stability, and social welfare.

Brief Discussion of FGS & Puntland Budgets for 2023

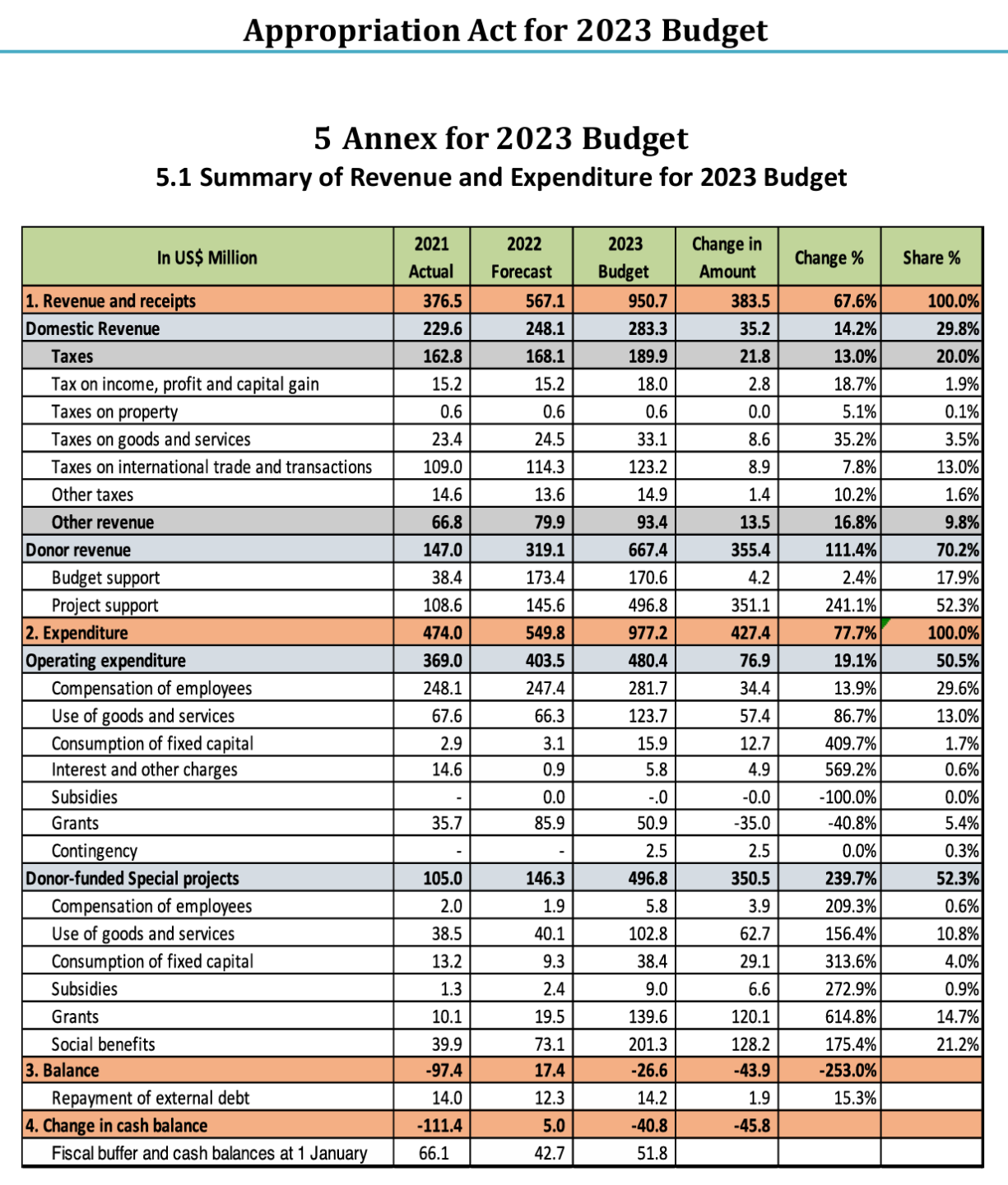

As attached in Appendix I, the budget for the Federal Government of Somalia for the period from January 1, 2023, to December 31, 2023, is projected to be US$950,661,544. This total includes government revenues and other funds, such as grants, amounting to US$637,355,405, which represents 67% of the total budgeted income. The primary source of revenue, aside from grants, comes from taxation, totalling US$189.9 million. However, the total domestic revenue is estimated to increase from $229.6 million in 2021 to $283.3 million in 2023, provided the proposed revenue measures are approved and successfully implemented. The total appropriated expenditure budget for both recurrent and projected expenses is US$977,216,539, netting a budget deficit of US$26,554,995.- In the fiscal year 2023, it is confirmed that the FGS is proposing to introduce touch expenditure measures such as Implementing internal audit function in all MDAs as well as implementing external audit recommendations to ensure all payments must have adequate supporting documents based on the Auditor General’s recommendations in the 2020 audit report.

It is worth noting that the 2023 FGS’s budget strategy will therefore need to address the key problems the country faces regarding implementation of NDP9 priorities to be able to achieve the NDP9 goals. The budget is designed to focus on how the government can exploit the opportunities for economic growth over the medium term (2023-2026) in terms of promoting regional trade by joining the EAC to improve access to regional markets, encouraging import substitution for some products that could be locally manufactured and continued pursuit towards the transformation of public service delivery to be more efficient and effective in meeting the needs of the people.

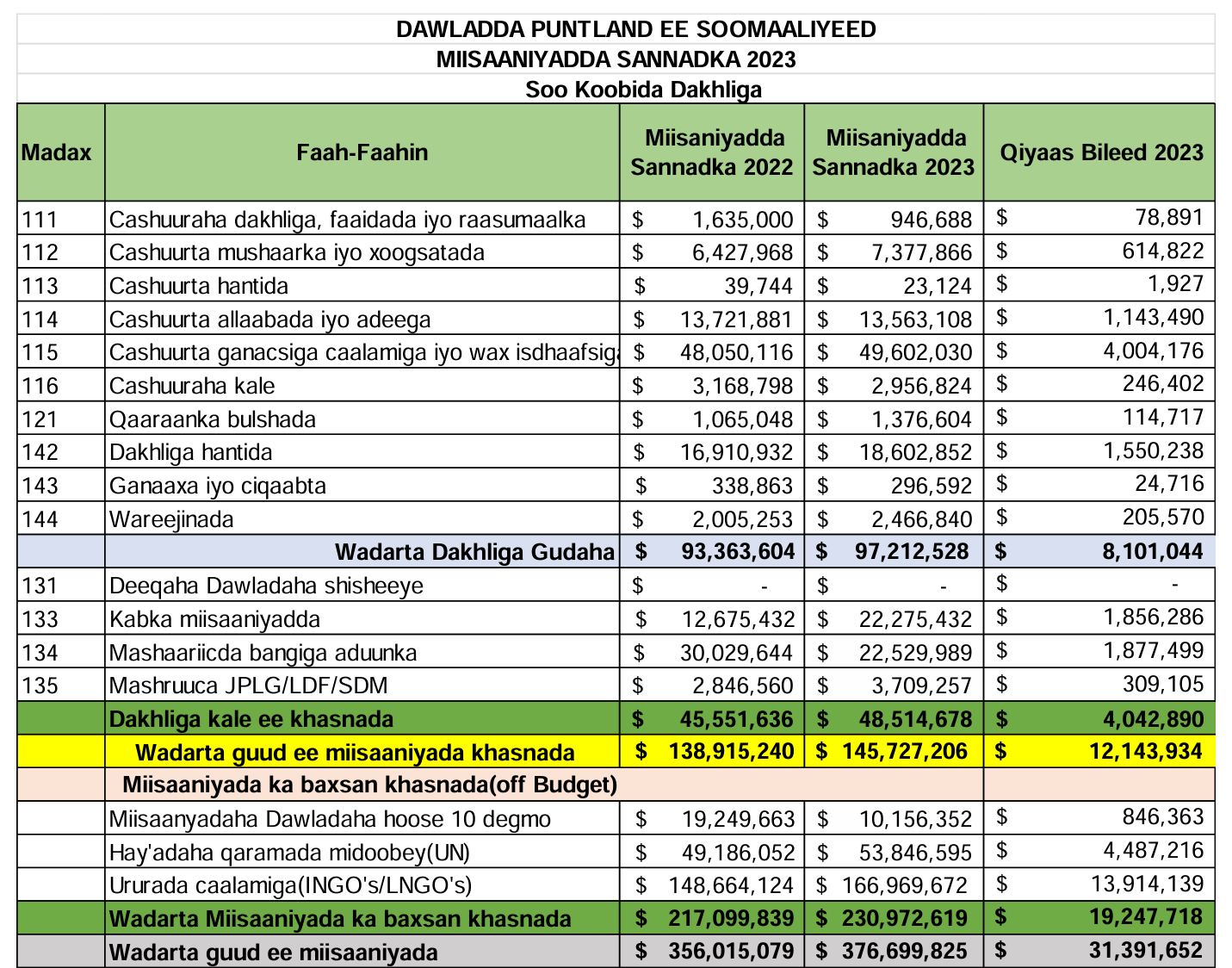

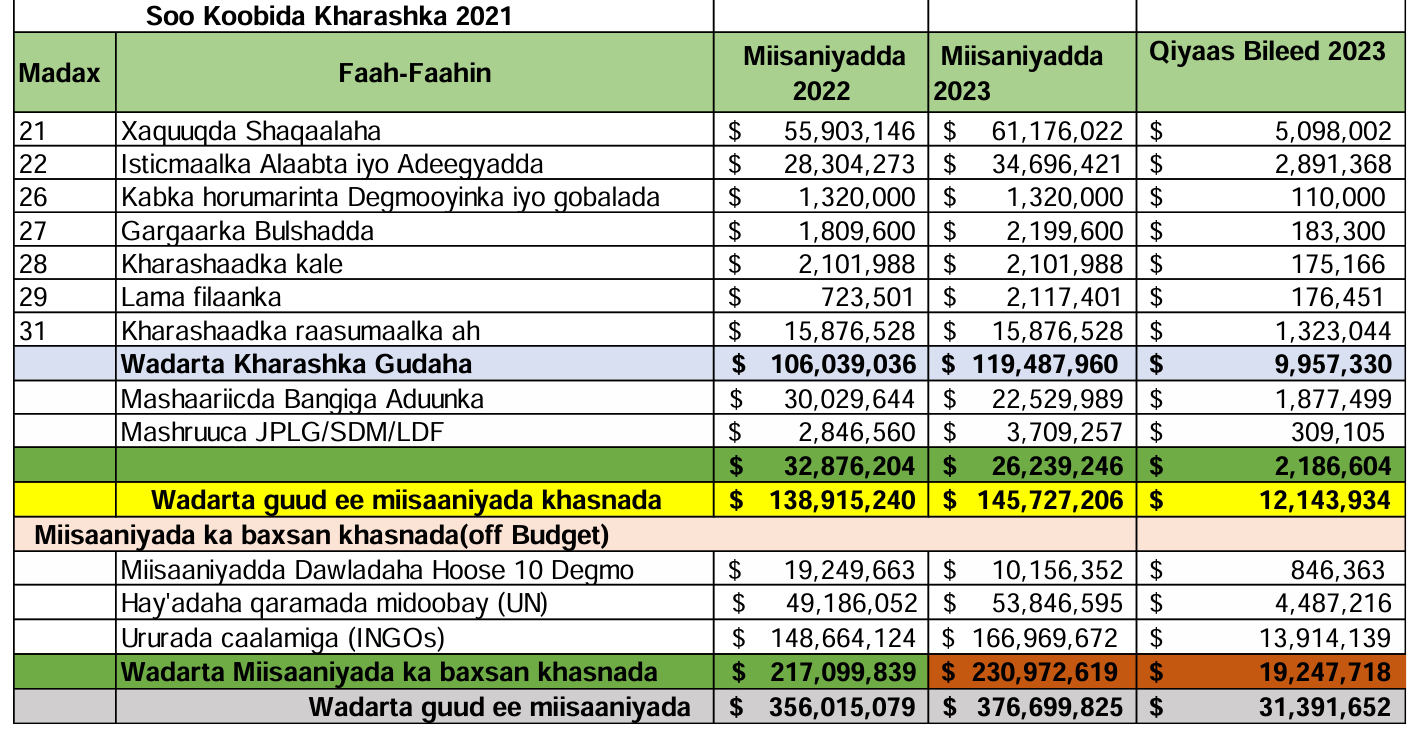

Likewise, Appendix II depicts the income budget for the Puntland State of Somalia, the largest FMS and the most resourceful, for the period from January 1, 2023, to December 31, 2023, which is projected to be US$376,699,825. This includes government revenues and other funds, such as grants and 10 main districts in the state. Grants including those funds managed by international partners amount to US$269,330,945 representing 71% of the overall income budget. In addition to grants, the primary source of revenue comes from taxation, totalling US$97,212,528. If you add that with the ten local districts, the total internally generated revenue is US$107,368,880. The budget also appropriates 100% of the projected income for both recurrent and projected expenditures with no budget deficit which indicates an unusual phenomenon.

Appendix I:

FGS budget Snapshot: Income/Expenditure 2023

Source: Federal Ministry of Finance

Appendix II:

Puntland budget: Expenditure 2023, Source: Puntland Ministry of Finance

Appendix III:

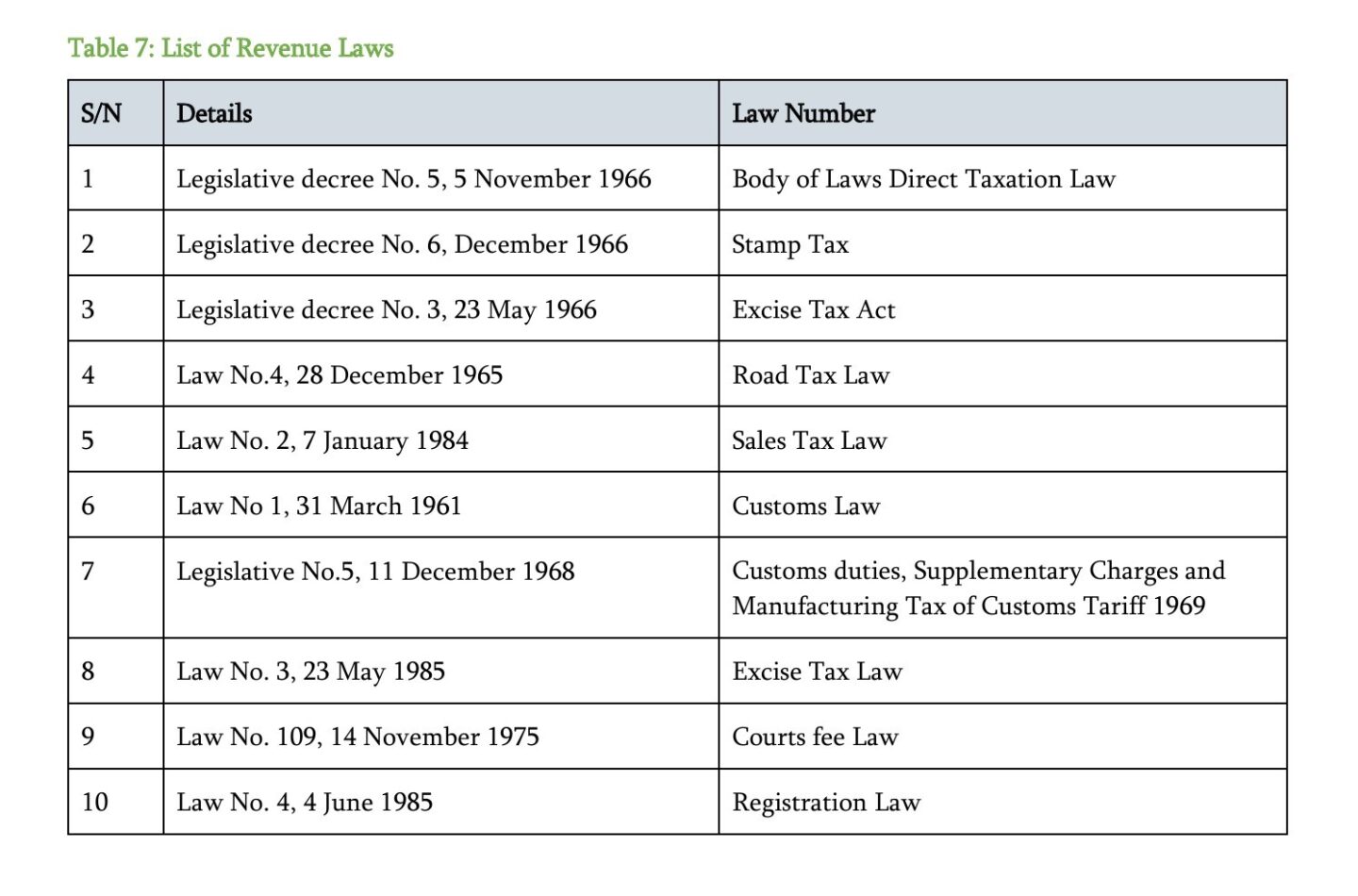

List of Revenue/Tax Laws:

References: